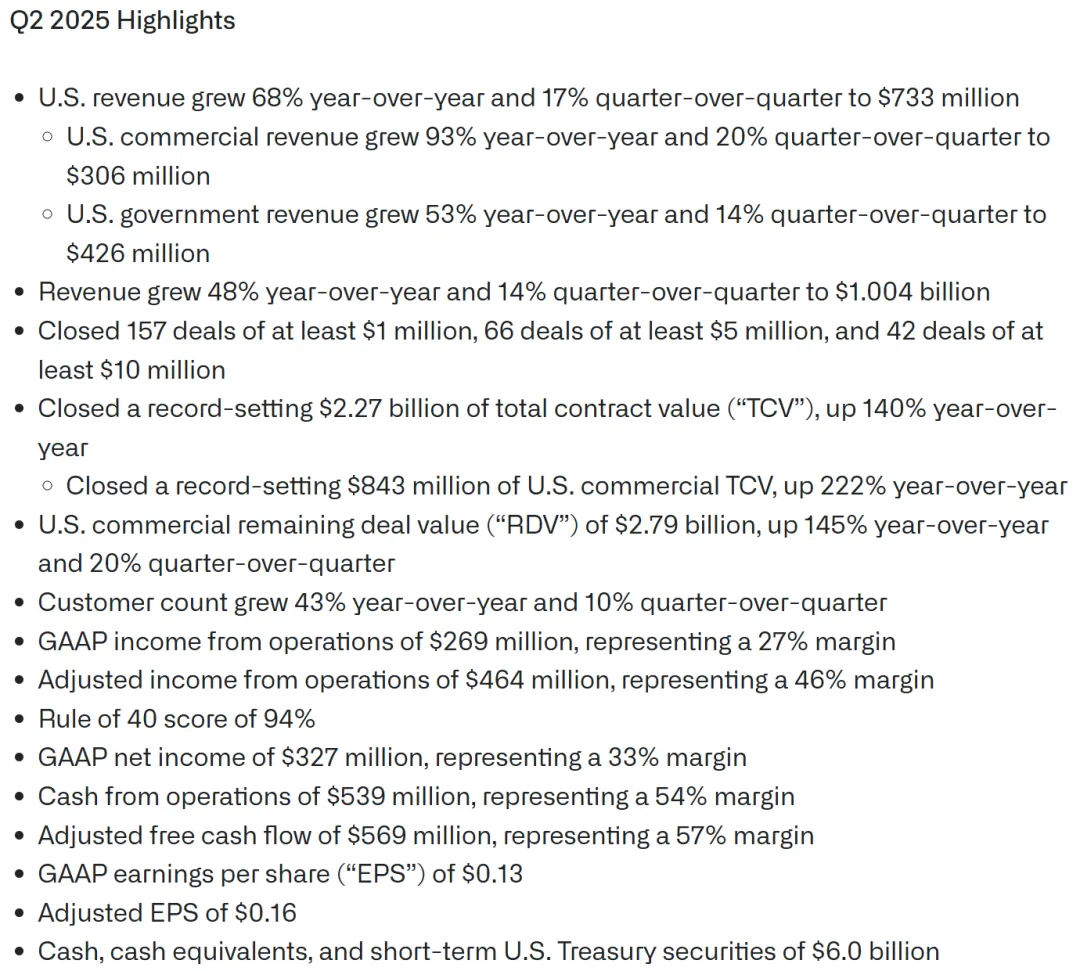

On Monday, August 4, after the US market close, Palantir (PLTR) reported Q2 2025 earnings, crossing the $1 billion quarterly revenue milestone for the first time. Results beat Wall Street expectations, driven by strong AI platform demand, especially from US commercial and government segments. The stock surged ~9% in after-hours trading to an all-time high.

Let's look at the customer and growth metrics:

-

Customer count: 849 total, +43% YoY; 485 US commercial, +64% YoY.

-

Net Dollar Retention (NDR): 128%, +400 bps QoQ, indicating increased spending from existing customers.

-

Remaining Deal Value: $7.1 billion, +65% YoY.

-

Remaining Performance Obligations (RPO): $2.4 billion, +77% YoY.

-

Rule of 40 score: 94, +11 points QoQ (growth rate + margin, measuring sustainable growth).

Growth is primarily driven by AI technology. For example, Citibank reduced customer onboarding from 9 days to seconds, Fannie Mae cut mortgage fraud detection from 2 months to seconds, and Nebraska Medicine improved discharge lounge utilization by 2100%.

Meanwhile, the company raised full-year guidance, reflecting sustained optimism for AI demand:

-

Q3 2025: Revenue $1.083-1.087 billion, +50% YoY, +8%+ QoQ.

-

FY 2025:

-

Total revenue: $4.142-4.150 billion, +45% YoY (above Wall Street's $3.91 billion estimate).

-

US commercial revenue: over $1.302 billion, +85% YoY.

-

Adjusted operating income: $1.912-1.920 billion.

-

Adjusted free cash flow: $1.8-2.0 billion.

(Source: Palantir Technologies) Breaking down PLTR's performance, Q2's red bar (revenue growth) accelerated vs Q1's comparison to Q4 last year. Adjusted Operating Margin returned to 46% growth, not declining to 44% as in Q1. The yellow line plus YoY Revenue Growth (Rule of 40) hit a record 94%, up from 83% last quarter. These metrics show PLTR is back in a high-growth phase, with Q2 earnings revealing stronger momentum.

(Source: Palantir Technologies, Mingtao HUANG) Looking at business segment breakdown (chart below), US government contracts remain the absolute majority of PLTR's revenue, followed by US commercial. However, non-US commercial revenue is declining in both share and absolute terms. For PLTR's lofty valuation, strong US performance alone may not suffice; growth in non-US operations is also needed.

(Source: Palantir Technologies, Mingtao HUANG) According to Yahoo Finance, PLTR has surged over 16x in the past 5 years, with a P/E TTM of nearly 600x and a static P/E over 900x. Even among AI companies in the star-studded US market, this valuation is extremely high. PLTR's stock price is also at historical extremes. This investment may suit only those with deep research into PLTR or strong conviction in the company. Future earnings will need to consistently blow past Wall Street expectations to sustain such a high valuation.

(Source: Yahoo Finance)

As the hottest AI application stock in the US market, I'll follow up with a deeper analysis of PLTR's business and moat. Although I've been drafting that article on and off for about a year, the more I write, the more I realize PLTR has many layers to uncover—not just business analysis, but also its philosophy, founder commentary, and the company's unique mission and positioning. Stay tuned.

Risk disclaimer: This content is for informational purposes only and does not constitute investment advice. Markets are risky; invest with caution.

If interested, feel free to follow for more.

专注投资分析、市场洞察与资产配置。不追短期波动,只理解真正驱动长期回报的东西。